2025 Off to Shaky Start for Multifamily

Provided by Jordan Brooks, Senior Market Analyst at ALN Apartment Data.

2024 was an encouraging year for Greater Dallas multifamily, but it was not without challenges. While the last few months have featured some positive developments, the opening month of 2025 provided a red flag that bears watching as the new year begins to unfurl.

All numbers will refer to conventional properties of at least fifty units.

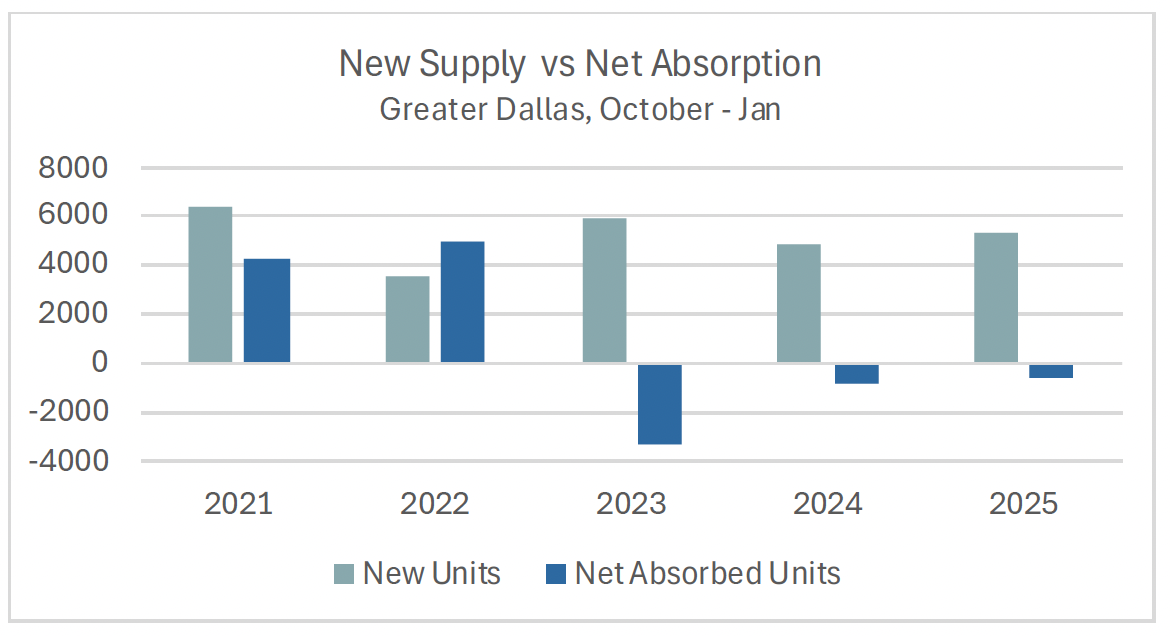

New Supply Remains Robust

An active new construction pipeline is nothing new for Greater Dallas, especially over the last handful of years. More than 5,300 new units were delivered across the market from the start of October through the end of January. That level of new supply was slightly higher than for the same period a year ago.

New supply will be a major force throughout 2025. New deliveries may total a few thousand units less than last year but about 15,000 new units are still expected to begin leasing. In the last five years, only 2021 net absorption surpassed that mark. As a result, new supply will likely be a headwind for occupancy again this year.

Apartment Demand Stumbled

Given the new supply picture, continued recovery in apartment demand will be vital this year for occupancy performance to be mitigated and for rent growth to return to its typical range. The final quarter of 2024 provided reason for optimism going into 2025. Not only had apartment demand been on a consistent upward trajectory since 2023, but fourth quarter net absorption last year was positive for the first time since 2021.

Unfortunately, January was a step in the wrong direction. A net loss of around 2,200 leased units in January was the largest monthly decline in years. It also wiped out all the gains from the final quarter of last year – and then some. Too much should not be taken from just one month of data.

However, the scale of the negative move was noteworthy. So too was the fact that the January result fit what occurred in the national data as well. A net loss of more than 38,000 leased units during the month across the country was similarly the largest single-month decline in years. January demand may end up being an outlier within an otherwise strong year. Even so, the opening month of the year presented a tenuous start to the year.

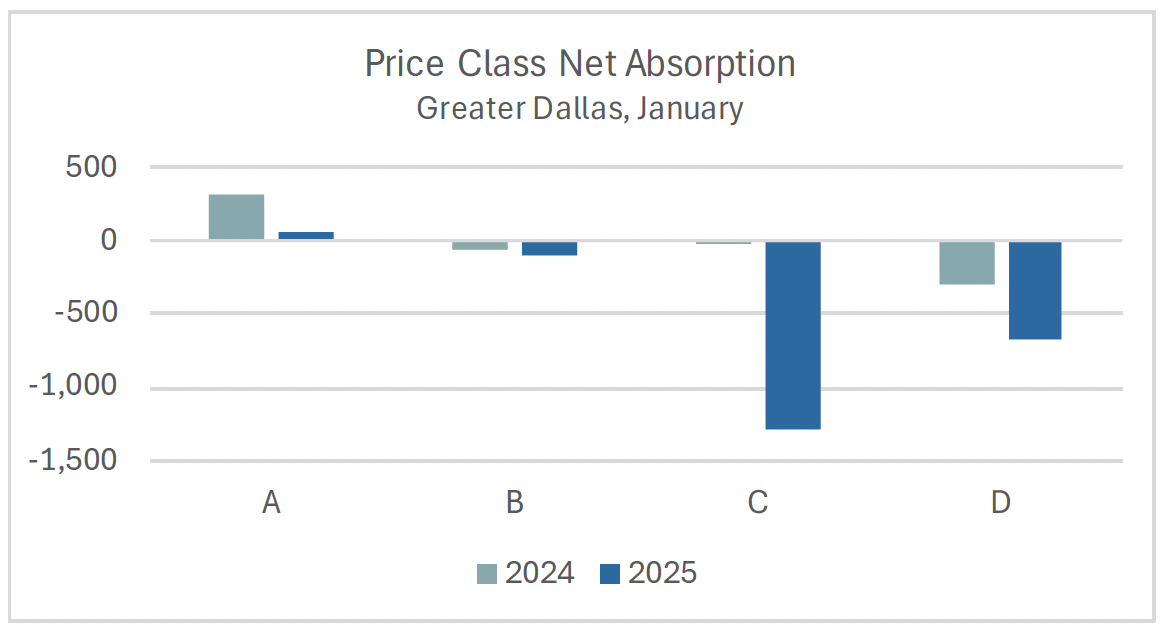

Price Class Demand Differences

Recent months have looked more like 2023 than 2024 for apartment demand when segmented by price class. Class A net absorption since the start of October has totaled approximately 1,500 units. That was the best mark for Class A for this portion of the calendar in more than five years – better even than the October 2021 through January 2022 period.

For Class B, a net loss of around 100 leased units in January brought the total over the last four months to less than 300 net absorbed units. The winter period is traditionally the weakest point of the year for apartment demand, but this total was the second lowest of the last five years for the period. The positive momentum that began in 2023 and grew in 2024 has dissipated even when accounting for seasonality.

The more troubling recent developments have come from the workforce housing segments of the market. Whereas the top of the market was already regaining its footing in 2023, Class C demand did not materially bounce back until last year. Class D still shed net leased units in 2024.

Since the start of the fourth quarter last year, Class C has returned to negative territory with a net loss of nearly 1,000 leased units over the last four months. Again, this period is generally tough for apartment demand. Even so, the result was worse than in the same period a year ago. Furthermore, just more than half of the market-level loss in January came from Class C properties.

Class D properties have shed more than 1,100 leased units over the last few months, including more than 600 net units in January. Going into 2025 there was reason to believe that this year could be the turnaround point for Class D demand. Plenty of time remains, but January was a rocky start for this segment.

Takeaways

Despite optimism coming into the year, 2025 has gotten off to an inauspicious start for Greater Dallas multifamily. As anticipated, new supply has remained active. Unfortunately, the positive trajectory in apartment demand that has been in place since the end of 2022 has softened.

Class A net absorption has been the most resilient, and this is helpful given the new supply. However, if the workforce housing segments take a step back this year, 2025 could more closely resemble 2023 than an improvement on 2024. However, the sky is not falling. One month of poor data does not make a trend. A better indication of where 2025 is headed will come once spring arrives.

*Jordan Brooks is a Senior Market Analyst at ALN Apartment Data. https://www.alndata.com

ALN is the largest collector of apartment data in the United States. We update property-level information monthly, reporting on properties nationwide, and provide our clients with data analytics, new construction projects, histories, occupancy and rental trend reports, contact databases and locating services.